AI tools were used in the research, drafting, and editing of this article. All factual claims are sourced to primary documents and verified by the author.

Residents in DeKalb and Sycamore have had understandable questions about how Meta’s data center and other recent developments affect property values, tax bills, and local budgets. With assessments rising and different taxing bodies making different levy decisions, it can be hard to make sense of what’s happening. This addendum consolidates actual county tax bills, public levy notices, parcel-level data, and Enterprise Zone documents to provide a clear explanation of what occurred between 2020 and 2024.

This article is part of the broader series “What Data Centers Actually Mean for Northern Illinois Communities”.It focuses specifically on property taxes – giving residents, officials, and skeptical readers a complete, source-rich breakdown of this topic without having to sift through the whole overview piece.

1. How Illinois Property Taxes Really Work

Illinois uses a levy-based property tax system.[68] Each taxing body – school district, city, park district, township, library, or county – decides how many dollars it needs for the year. The tax rate is then determined automatically:

Rate = Levy ÷ Equalized Assessed Value (EAV).[68][69]

Your tax bill depends not only on your home’s EAV but also on the total EAV of the whole taxing district. When the tax base grows, the same levy can be shared across more value, which lowers the rate and reduces the burden for each resident.[70, “How Rates Are Set”]

This is why large commercial and industrial projects can meaningfully shift the tax load.

2. What an Enterprise Zone Abatement Actually Is

An Enterprise Zone abatement does not refund taxes and does not give money back to a company. It temporarily discounts only a portion of the new value created by the improvement through new construction.[74, “Property Tax Abatement”][75, Subpart J §§520.1000–1030]

Land and pre-existing improvements remain fully taxed. Only a portion of the new value is abated for a fixed period.

A simple way to think about it: Collecting 50% of something is better than collecting 100% of nothing.

Without the project, that new value – and its revenue – would not exist. With it, communities receive millions in new dollars even during the abatement period.[70, FAQ #4]

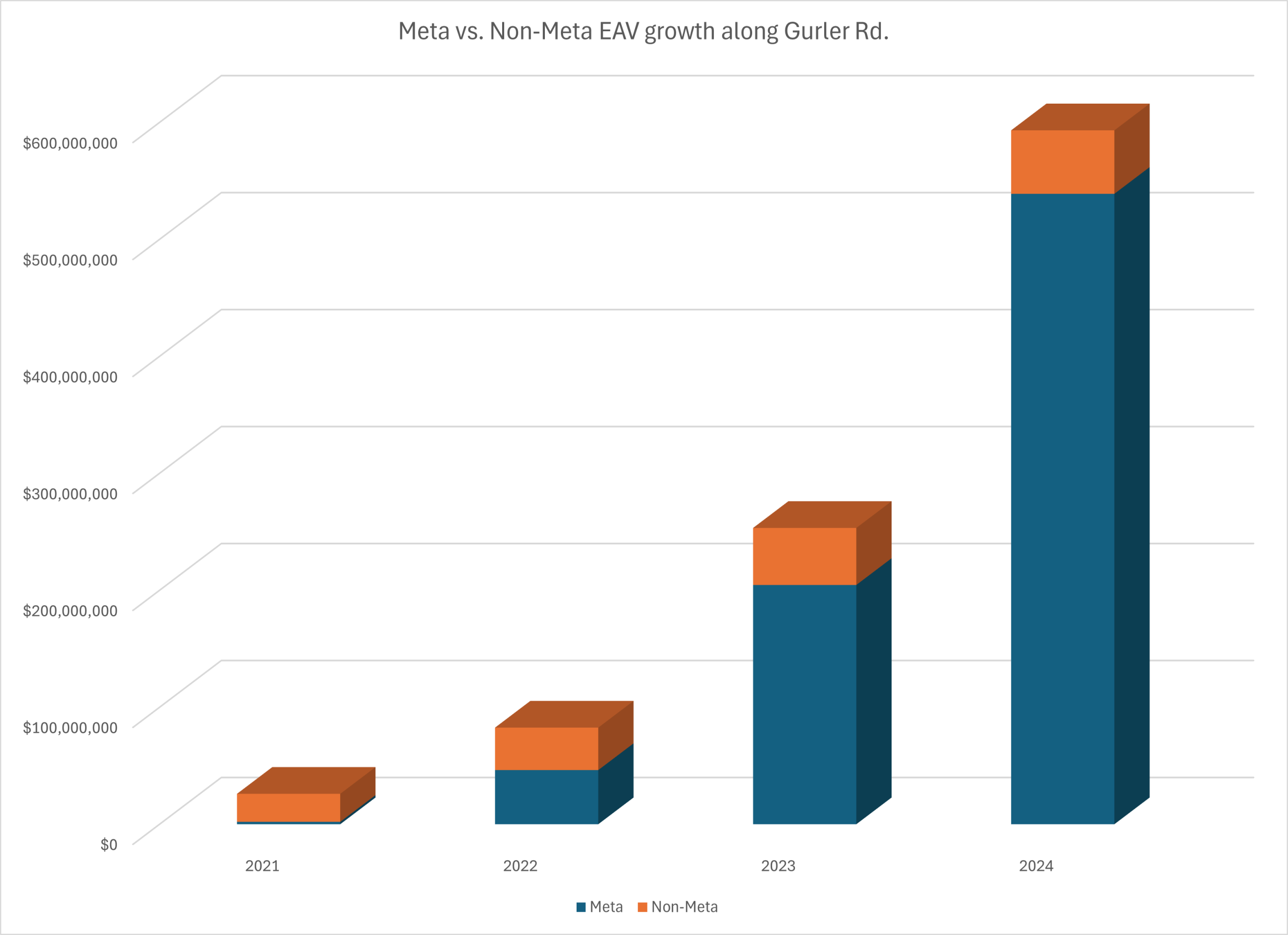

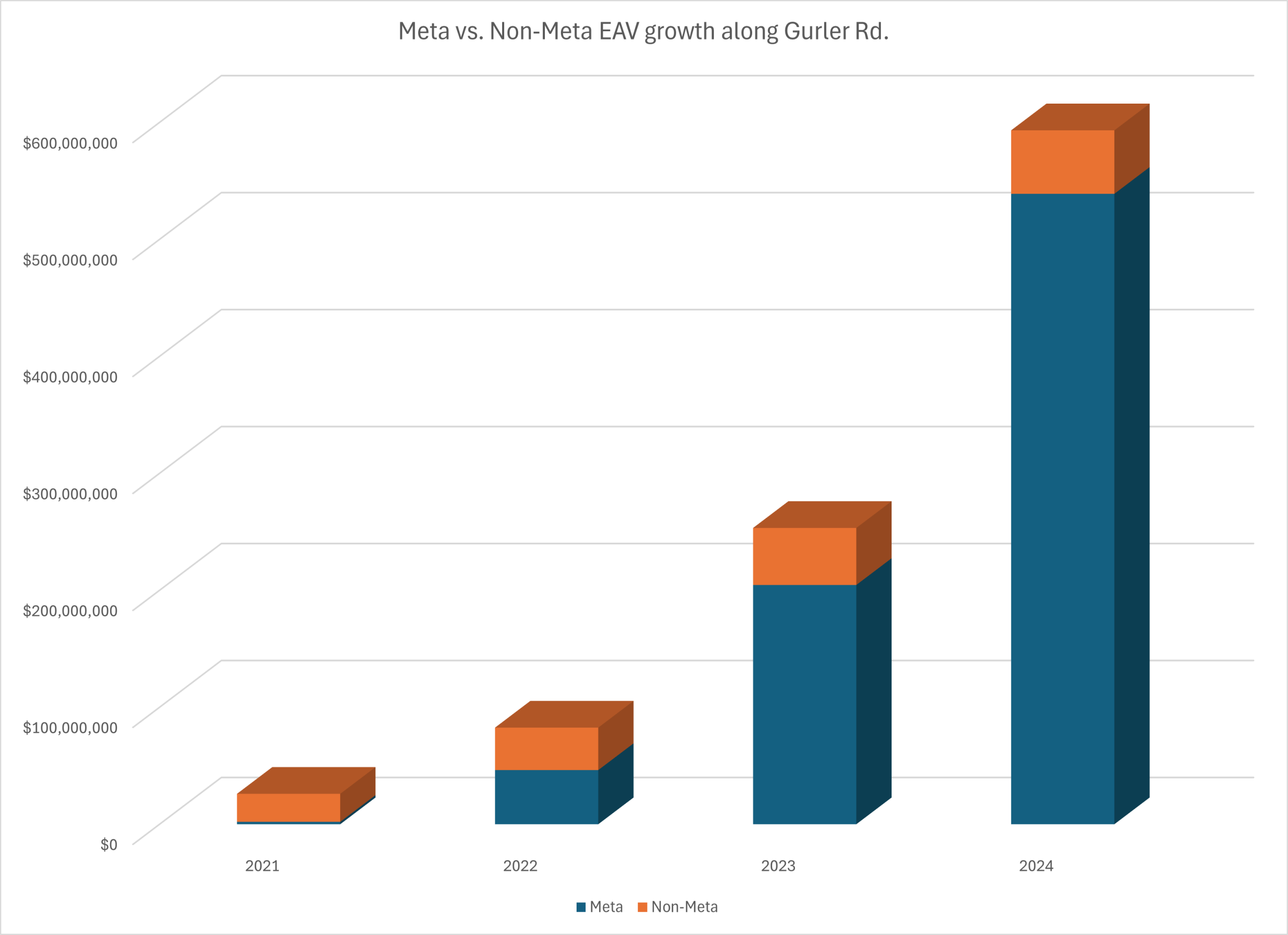

3. Meta’s Actual Taxes Paid in 2024

Three Meta parcels were fully on the 2024 tax rolls:

Parcel 11-01-100-004 • EAV: $531,240,341 • Total tax: $31,458,804.32[71]

Parcel 11-02-200-004 • EAV: $7,362,771 • Total tax: $587,162.06[72]

Parcel 11-01-100-005 • EAV: $333,896 • Total tax: $26,627.36[73]

Total paid by Meta in 2024: $32,072,593.74

Approximately $19.43 million went to School District 428 (derived from taxing-body splits in [71]–[73]). Another $12.64 million was allocated to the City, County, Park District, Library, Township, Kishwaukee College, and other entities.

These are actual numbers already reflected in local budgets.

4. Meta’s Abatement in Context

The 2024 Enterprise Zone report confirms: • 55% abatement on new improvements • 20-year schedule beginning with 2024 taxes[76, p. 2]

The abated amount on the main parcel’s new improvement value in 2024 was approximately $10.9 million. Without abatement, the total potential would have been roughly $42 million across the phased schedule.[76, p. 3]

Yet, Meta still paid approximately $31.5 million for the main parcel in 2024.

Even with abatement, Meta is one of the largest taxpayers in northern Illinois.

5. DeKalb vs. Sycamore: What Actually Happened to Homeowners (2020–2024)

Nearly all parcels saw EAV increases due to market conditions:[82] • DeKalb: 97.9% of parcels increased • Sycamore: 97.3% of parcels increased

But tax bills diverged sharply:

Parcels where total tax decreased: • DeKalb: 81.5% • Sycamore: 11.2%

Detailed movement (EAV ↑/↓ vs Bill ↑/↓), using 2020–2024 parcel-level data:[82]

DeKalb • EAV↑ & Tax↓: 7,813 parcels (73.2%) • EAV↑ & Tax↑: 1,820 parcels (17.0%) • EAV↓ & Tax↓: 93 parcels • EAV↓ & Tax↑: 1 parcel

Sycamore • EAV↑ & Tax↓: 803 parcels (10.1%) • EAV↑ & Tax↑: 6,375 parcels (79.9%) • EAV↓ & Tax↓: 45 parcels • EAV↓ & Tax↑: 0 parcels

The difference is largely due to DeKalb’s rapidly expanding commercial/industrial tax base – Meta, Ferrara, Amazon, and others in District 428 – versus Sycamore’s comparatively slow growth.[82]

6. The City of DeKalb’s Proposed Levy Increase

Official City notice for 2025 shows:[77]

• Levy increase: 7.65% • EAV increase: 7.65% • Tax rate: 0.62286 → 0.62284 (essentially flat)

When levy and EAV rise together, the rate stays stable. New commercial/industrial EAV absorbs the increase.

7. The Park District’s 2025 Proposal and Long-Term Trend

Park District’s 2025 notice:[78]

• Levy increase: 8.03% • Rate increase: 0.49147 → 0.55090 (~12.1%)

Their example shows the Park District line on a ~$300k home rising from ~$511 to ~$633.

However, context matters: From 2019 to 2024, the Park District tax rate decreased by 32%, from 0.72045% to 0.49147%, as the EAV more than doubled.[79]

Even with the proposed 2025 increase, the rate remains 23% lower than in 2019.

8. Why Some Individual Bills Still Rose

Even when a district experiences a strong rate compression overall, individual bills may rise when:

• A particular home’s EAV increases faster than average • Improvements were added • Exemptions changed • Smaller taxing bodies increased levies faster than their EAV rose[70, “Why Bills Vary”]

These are individual circumstances – not contradictions of the multi-year pattern.

9. What This Addendum Does Not Claim

This addendum does not claim: • that taxes never rise • that abatements have no cost • that large taxpayers eliminate levy increases • that every homeowner saw the same outcome

It reports on what occurred from 2020 to 2024, using actual tax bills and official documents.

10. A Call to Action

Residents can request that their taxing bodies provide clearer levy/EAV explanations, side-by-side comparisons, and plain-language breakdowns of how new construction affects tax rates.

Taxing bodies can improve transparency by providing simple levy/EAV charts and clean explanations of each line item.

11. Closing Thoughts

Between 2020 and 2024, DeKalb added hundreds of millions of dollars of new commercial and industrial EAV.[82]

Meta alone contributed more than $32 million in taxes in 2024.[71–73]

This expanded base allowed District 428 and others to maintain necessary revenue while lowering tax rates, resulting in most DeKalb homeowners seeing lower tax bills even as assessments rose.

Sycamore, without similar development, experienced the opposite trend.[82]

The multi-year pattern is clear: When more value shares the load, homeowners benefit.

Methods & Transparency

I utilize a range of AI and automation tools, in conjunction with my own research, to organize and verify complex public data – from DeKalb County tax rolls and DevNet parcel records to PJM TEAC maps and ComEd reliability filings. ChatGPT has been the primary workhorse for synthesis, but I also utilize Copilot, Gemini, Claude, and Grok to cross-check facts, refine tone, and develop Python-based tools for analysis. Grammarly keeps the writing clear – I use it for nearly everything I write, even texts.

Over the past several months, I’ve invested well over 100 hours reviewing, verifying, and refining this information. I have also permanently archived more than 100 key source documents in the Internet Archive’s Wayback Machine to ensure transparency and durability. The work is still ongoing as new filings and community feedback come in.

Every figure and citation is sourced from public records that you can verify independently. My goal is to make complex infrastructure and taxation topics accessible and understandable to everyone in the community. I’m just a local guy with a day job and a family, trying to make the public data we already have a little easier for everyone to understand.

This article is part of the Data Centers: The Public Record series. View all technical analysis →

[68] Illinois Department of Revenue – PTAX-60 Property Tax Rate and Levy Manual https://web.archive.org/web/20250728002219/https://tax.illinois.gov/content/dam/soi/en/web/tax/research/publications/documents/localgovernment/ptax-60.pdf

[69] 35 ILCS 200 – Property Tax Code (Art. 18, §18-50) https://web.archive.org/web/20251115214636/https://www.ilga.gov/Legislation/ILCS/Articles?ActID=593&ChapterID=8&SeqStart=6700000&SeqEnd=8000000

[70] DeKalb County Finance Office – Property Tax Levies & Rates (“How Rates Are Set,” “Why Bills Vary,” FAQ #4) https://web.archive.org/web/20240723184239/https://dekalbcounty.org/departments/finance-office/financial-tax-information/property-tax-levies-rates/

[71] DevNet – Parcel 11-01-100-004 (2024 Tax Bill) https://web.archive.org/web/20251115143744/https://dekalbil.devnetwedge.com/parcel/view/1101100004/2024

[72] DevNet – Parcel 11-02-200-004 (2024 Tax Bill) https://web.archive.org/web/20251115143737/https://dekalbil.devnetwedge.com/parcel/view/1102200004/2024

[73] DevNet – Parcel 11-01-100-005 (2024 Tax Bill) https://web.archive.org/web/20251115144001/https://dekalbil.devnetwedge.com/parcel/view/1101100005/2024

[74] Illinois DCEO – Enterprise Zone Program (“Property Tax Abatement”) https://web.archive.org/web/20251115210754/https://dceo.illinois.gov/expandrelocate/incentives/taxassistance/enterprisezone.html

[75] 14 Ill. Adm. Code Part 520 – Enterprise Zone Rules (Subpart J §§520.1000–1030) https://web.archive.org/web/20251115210753/https://www.ilga.gov/agencies/JCAR/EntirePart?titlepart=01400520

[76] DeKalb County – Enterprise Zone Abatement Report, Tax Year 2024 https://web.archive.org/web/20251115144040/https://dekalbcounty.org/wp-content/uploads/2025/05/tr-ez-abatement24-25.pdf

[77] City of DeKalb – 2025 Proposed Property Tax Levy Increase Notice https://web.archive.org/web/20251115211405/https://www.cityofdekalb.com/DocumentCenter/View/19994/9-2025-BBN-Pub-110125

[78] DeKalb Park District – Truth in Taxation 2025 https://web.archive.org/web/20251115210919/https://dekalbparkdistrict.com/news/truth-in-taxation-2025

[79] DeKalb Park District – Tax Levy & EAV Historical Summary (2019–2024) https://web.archive.org/web/20251102171237/https://dekalbparkdistrict.community.highbond.com/document/13a4a189-cf56-4454-938f-ba9ef5a28ade/

[80] Supervisor of Assessments – Annual Report 2022 (p. 7: abatement applies only to new construction) https://web.archive.org/web/20240714172127/https://dekalbcounty.org/wp-content/uploads/2023/05/ao-annrpt-2022.pdf

[81] DevNet public lookup landing page https://web.archive.org/web/20251115212527/https://dekalbcounty.org/departments/treasurer-collector/

[82] DeKalb County Treasurer – parcel-level EAV/tax datasets for 2020–2024 (via data request; public lookup at dekalbil.devnetwedge.com) https://web.archive.org/web/20251115212527/https://dekalbcounty.org/departments/treasurer-collector/